Determining the best legal structure is key for every CPA practice’s business model. An accurate accounting firm LLC vs LLP comparison will help them find the difference between the liability, taxation, and management. Although both give limited liability, the structure and regulatory treatment can differ substantially.

The industry of accounting firms is a regulated one. State boards of accountancy regularly impose formation requirements. In specific states, registered Limited Liability Partnership or Professional Limited Liability Company is a must.

This choice is not only legally okay, it’s also smart. It impacts the distribution of profits, decision-making processes, and overall risk management strategies. An organized partnership can improve operational clarity and protect partners from unnecessary exposure.

This guide we will break down the differences in liability, taxation, management structure and practical criteria to select. By the end of this Business Guide, you will know which entity is best suited to the objectives of your firm and compliance requirements.

Basics of LLC and LLP You Should Know

A good accounting firm LLC vs LLP comparison starts with defining what each entity means. Both LLPs and LLCs are designed to protect limited liability. Yet, they are not similar in foundation.

Limited Liability Partnership is an improved form of partnership. This lets partners steer clear of personal responsibility for the negligence committed by others. Each partner is responsible for his/her own profession.

A Limited Liability Company combines elements of partnership and corporation. Members are protected from business debts and operational failures. An LLC will have flexible governance arrangements.

| Feature | LLP | LLC |

|---|---|---|

| Ownership | Partners | Members |

| Liability Shield | Protects from other partners’ negligence | Protects from business debts |

| Management Style | Partner-managed | Member or manager-managed |

| Professional Use | Common for CPA firms | Often requires professional designation |

LLPs are often preferred by accounting firms due to their partnership structure. Nevertheless, frameworks of Professional LLC have become common.

Check your state’s licensing requirements before forming either entity. CPA ownership in some jurisdictions reserved for licensed professionals. Always prioritize compliance above all.

Protection from liabilities and rules

Usually concerned about liability accountants emphasize LLC vs LLP. The client advice and financial reporting tasks cause a professional risk to the accounting practice.

Partners are not liable for another partner’s wrongdoing in a limited liability partnership. This safeguard encourages working together but limits exposure. Nonetheless, personal malpractice is the individual professional’s responsibility.

In an LLC the members are shielded from debts and obligations at the company level. Members remain personally liable for their own professional negligence, as is the case with an LLP .

A Look At Professional Licensing

CPAs must register with state boards as professional entities. This involves creating a Professional Limited Liability Company or registering as a Professional LLP.

There could be ownership restrictions. Only licensed CPAs may be an owner in some states. The standards are in place to ensure professionalism and trust by the public.

Imposing penalties or suspension to deal with those regulations’ violations. The selection of entities must comply with state regulations.

Risk and Insurance Management

No matter the form, malpractice insurance is a must. Professional risk remains despite limited liability. Having insurance will give you the coverage you need.

Consider when evaluating regulation requirements

- Approval from the State Board professional entities.

- Eligibility criteria on ownership.

- Compulsory malpractice coverage.

APRA Reporting and annual renewal golden rules

It is mandatory for both LLPs and LLCs to stay in good standing with the Secretary of State. Submissions on time safeguard rights.

Being aware of the differences in liability helps make better choices. Expert counsel usually clarifies state-specific issues.

Tax Treatment and Operational Structure

There’s another paramount factor that you must not underestimate in an accounting firm LLC vs LLP comparison. And that is taxation. Both typically enjoy benefits of pass-through taxation. Corporate-level income tax is avoided.

Profits and Losses in an LLP Pass Directly to Partners. Every partner must report his share on his tax return. This set-up makes tax reporting easy.

An LLC also defaults to receiving pass-through taxation. But it can choose corporate tax status if advantageous. This flexibility can certainly underpin long-term planning.

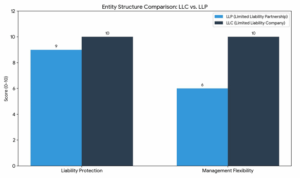

- The governance of LLC is more adaptable and flexible as compared to LLP. The scores of the partnership model of LLP are low because it continues with the conventional model of partnership. In this LLC scores 10/10 while LLP scores 6/10.

- Both provide robust safeguards for their owners and managers from liability associated with company debts and torts. Yet, the LLC essentially offers a slightly more comprehensive form of protection: a 10/10 Broad Business Shield, compared to a 9/10 Partner-Focused Shield. The latter is usually only available for professional service businesses (e.g., medical, legal, etc.).

- Professional vs. General Use: The LLP structure is often preferred by professional practices (law or accounting firms) so that partners are not liable for the malpractice of other partners. The general commercial venture usually prefers the LLC as it offers maximum operational flexibility.

Here’s how to choose between an Accounting Firm LLC vs LLP

Choosing the right structure takes careful consideration. State professional licensing regulations begin volume. Verify which entities may engage CPA firms.

Examine your company’s business style. An foreign LLP may suit partners who prefer equal decision-making power. An LLC may be preferable for those looking for flexibility.

Have long term goals in mind Are you going to increase your market to multiple states? Will there be any shifts in ownership? Flexibility of the entity affects growth.

Carefully consider before you decide – Accounting Firm LLC vs LLP

- Requirements set by the state.

- Management structure desired.

- Plans relating to tax.

- Willingness to risk and implications.

After you select an entity, filing of formation and obtaining of the required approvals. Sign up with the state board of accountancy if required.

Continue to comply through annual reports and license renewals. Good record-keeping can boost legal shield.

Choosing carefully at the outset avoids costly restructuring. When things are clear, they run better.

Final Thoughts on Accounting Firm LLC vs LLP

When you compare accounting firm LLC vs LLP, both have their respective benefits. They both provide liability protection and pass-through taxation. However, the best choice is often determined by governance style and regulatory compliance.

Professional partnerships seeking equal authority usually form LLPs, while the management frameworks of LLCs are adaptable and flexible. Your choice may ultimately be influenced by state rules and regulatory requirements, and consulting services like Corporation Center can help guide businesses through the formation and compliance process.

When you plan carefully, you can get your entity structure in place. The firm must comply with licensing boards throughout its life.

Ultimately, choosing an entity type is more than just a paperwork issue. It affects your accounting firm’s liability, taxation and growth management. By thoughtfully assessing regulatory necessities and strategic objectives, you lay the groundwork for sustainable, long-term professional success.